Understanding the global oil shock

The current oil shock stemming from the closure of the Strait of Hormuz “constitutes the most severe flows and supply disruption in the history of oil markets”, according to a report from the Oxford Institute for Energy Studies. Gareth Hamill writes.

The Anatomy of the Strait of Hormuz Oil Shock explains that what sets the current global oil shock apart from previous crises is its sheer magnitude.

The Strait of Hormuz has been largely blocked by Iran since 28 February 2026, following US and Israeli airstrikes on Iran and the assassination of their Supreme Leader, Ali Khamenei.

In 2025, an average of 20 million barrels per day (mb/d) passed through the strait, which represents about 25 per cent of global oil exports.

The continued closure of the strait alongside Iranian attacks on critical oil infrastructure in Saudi Arabia, Qatar, and the UAE, some of the largest oil exporters in the world, transformed what was initially a flow shock into a production shock.

Crude oil production from the Middle East’s six biggest oil producers fell from 26 mb/d in February 2026 to 15 mb/d in March 2026. This is a 42 per cent decrease, which is the largest month-on-month supply disruption in the history of the global oil market.

Buffers

In addition to creating an oil shock, the disruption to the Strait of Hormuz has also eroded the effectiveness of a key mitigation mechanism available for oil markets: spare capacity.

This is the maximum volume of production that can be brought online within 30 days and sustained for at least 90, and it is one of the market’s most effective adjustment tools to shocks.

However, countries in the Middle East hold the majority of the world’s spare oil production capacity and are therefore constrained by the blockade of the strait.

The report also highlights that another buffer against shocks, strategic oil stocks, is extremely limited and can only act as short-term relief.

Member countries from the International Energy Agency (IEA) agreed to release 398 million barrels of their total 1.8 billion supply from their strategic petroleum reserves in March 2026 to mitigate production shock.

However, cumulative output losses are projected to have reached around 790 million barrels, almost twice the release of the IEA, by the end of April 2026, only two months after the start of the war.

Due to the magnitude of the production loss and the unavailability of spare capacity, the existing buffers are insufficient to replace the volumes of lost barrels, and if the blockade persists, these buffers will become even less effective.

A large demand reduction is needed to accompany the global supply issues, and this is already occurring with the IEA now projecting a small demand contraction of 80,000 barrels a day for 2026.

However, a large reduction in demand for oil is complicated by two issues.

Firstly, given the magnitude of the supply shock and because short-run oil demand is relatively price inelastic, the price would need to move incredibly sharply in order to generate the necessary demand response.

To match the global supply loss estimated to have occurred in March 2026, the report calculates that a price increase of 115 per cent would be necessary. Brent prices, the primary benchmark for international oil trading, rose by 46 per cent in March 2026 compared to February.

Second, the size of the current supply shock would require a demand response of comparable magnitude, which has rarely been seen in modern oil market history.

The report also forecasts that recovery from this crisis will “take months and is unlikely to be uniform across countries”.

Saudi Arabia is best placed to achieve the fastest and most complete recovery to pre-war output levels because of its large amount of technical and financial resources as well as its access to the East-West pipeline which bypasses the Strait of Hormuz.

Due to its lack of bypass options combined with infrastructure and export bottlenecks, the report highlights that Iraq is in the weakest position for recovery of all major oil producers.

Oil prices

The current shock is occurring in the context of “highly financialised and futurised oil markets”, as traders take speculative positions on the price of oil.

Financial trading on the market is larger than the underlying production and consumption of oil and plays a key role in price discovery, meaning prices rise higher than the physical shortage alone would imply.

The shock massively increased price volatility and uncertainty, which meant that the markets attracted a new set of financial players into the options markets.

Demand for call options surged. These benefit from an increase in the underlying asset’s price, as the supply shock increased the demand for insurance against higher prices.

The ability of option dealers to meet this demand was limited, and as insurance against further price increases, many of them bought futures, contracts to buy oil at a set price at a future date, meaning they would profit if oil prices continued to rise.

This increased demand for futures means that their prices also rose, and because futures markets are the main benchmark used to price physical oil this also rose to align with the future valuation.

This increase in oil prices created further demand for call options, creating a feedback loop which results in sustained increases in oil prices that will only be rectified by external actions which stop the supply shock, in this case, the re-opening of the Strait of Hormuz.

The impact of this current shock and the resulting market trading on oil prices has been enormous.

On 27 February 2026, the day before the war began, the Brent crude oil price per barrel was $73 and reached a peak of $110 on 30 April 2026.

This price has been incredibly volatile, with intermittent ceasefires and pauses in the blockade of the strait resulting in minor decreases

However, these measures have not lasted long enough to have a prolonged effect on oil prices, which are still significantly higher than they were pre-war and sit at $99 a barrel on 7 May 2026.

This has largely been the result of mixed signals from the US and its President, Donald Trump, who has repeatedly threatened Iran with destruction only days before committing to negotiations.

There appears to be a pattern of Trump making threats while the markets are closed on Fridays and Saturdays before announcing progress in negotiations as markets open on Sunday night or Monday morning.

On Saturday 21 March 2026, Trump wrote on Truth Social that if Iran did not “FULLY OPEN, WITHOUT THREAT, the Strait of Hormuz, within 48 HOURS”, the US would “obliterate” its power plants.

Then, on 23 March 2026, two hours before US stock markets open, Trump wrote that the US and Iran held “VERY GOOD AND PRODUCTIVE CONVERSATIONS REGARDING A COMPLETE AND TOTAL RESOLUTION” to hostilities.

At the same time, he also announced a five-day pause in strikes on Iran which coincided exactly with the opening times of the markets.

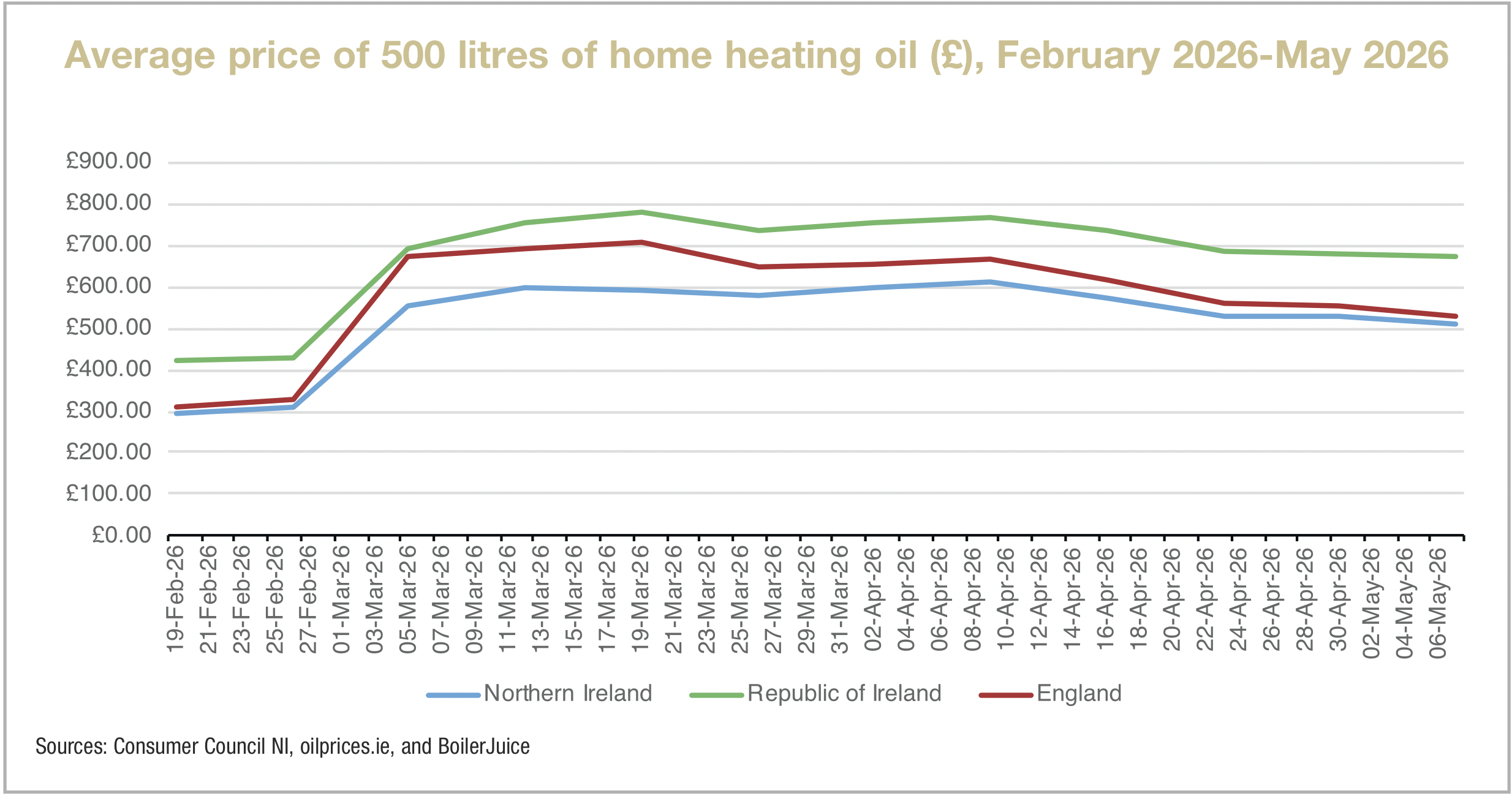

Local impact

Northern Ireland has been particularly affected by the price rises because of the high proportion of households that rely on oil to heat their homes.

In Northern Ireland, 62.5 per cent of households use oil for their heating compared to around only 5 per cent in Britain, and 26 per cent in the Republic.

On 26 February 2026, two days before the Strait of Hormuz was closed, the average price for 500 litres of home heating oil in Northern Ireland was £307, that price then rapidly rose and reached a peak of £612 by 9 April 2026, a 99 per cent increase in 6 weeks, according to the Consumer Council for Northern Ireland.

This prompted the Executive to approve a £100 payment for lower-income households to go towards their heating oil bills in April 2026.

The price has been steadily declining since that peak and, at the beginning of May 2026, sits at £510 for 500 litres, which is still a 66 per cent increase from the week before the war.

The continued uncertainty surrounding the war between Iran and the US means that the oil markets will remain volatile, and it will be some time before a return to pre-war oil prices.