Economic risks ‘especially pronounced’ for certain areas amidst energy transition efforts

The concentrated nature of fossil fuel generation sites means that possible job losses in the well-paid electricity sector could “present a troubling cocktail of factors impeding transition efforts”, a new report has found.

This contention is made in a recent report by the Nevin Economic Research Institute (NERI) that explores the idea of a “spatially just transition” and maps regional risk associated with the transition away from fossil fuels towards a system of “electrifying everything” and decarbonising electricity, with emissions reductions of 75 per cent from 2018 levels and 73 per cent from 1990 levels targeted in the Republic and Northern Ireland respectively.

“Fossil fuel generation sites generating emissions are relatively concentrated in specific regions,” the report, written by Paul Goldrick-Kelly and Jonas Poulsen states. “This relative concentration and spatial distribution of sites, which will have to undergo some form of change if we are to meet our [all-island] emissions reductions goals, raises issues of spatial capacity and justice in relation to transition.”

Amid this assertion, the authors pose the question: “If transition must occur at these sites, which may imply closure, are these areas equipped to deal with the economic and social effects?”

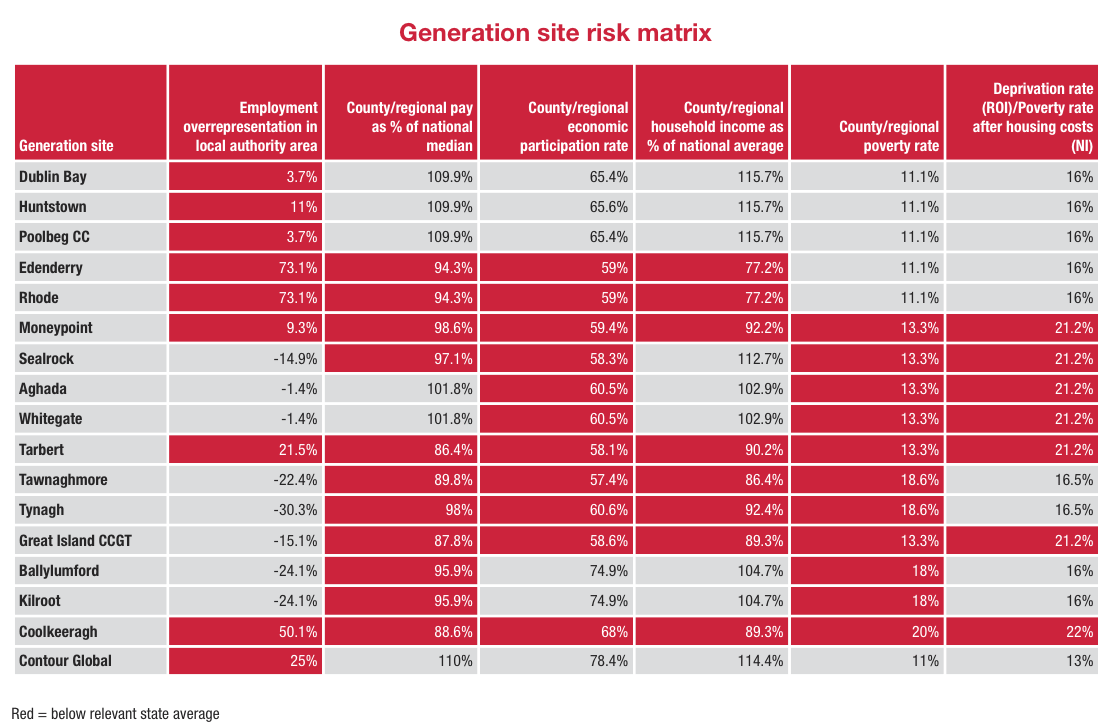

Using the generation capacity statement for the all-Ireland grid, the report identifies the key fossil fuel generation sites across Ireland as: Edenderry; Rhode; Moneypoint; Sealrock; Tawnaghmore; Tarbert; Great Island CCGT; Tynagh; Aghada; Whitegate; Dublin Bay; Poolbeg; Huntstown; Coolkeeragh; Ballylumford; Kilroot; and Contour Global at Knockmore Hill, Lisburn. The sites with the highest generation capacity in both jurisdictions were Moneypoint, generating 855MW in the Republic and Ballylumford, generating 709MW in Northern Ireland.

Changes are already afoot in the electricity sector, as the report notes. The 476MW generated by two steam turbines on heavy fuel oil and coal in Kilroot, County Antrim ceased operations in September 2023; Tarbert power plant in County Kerry is due to close its 592MW of gas and distillate oil-powered electricity to make way for a 350MW open cycle gas turbine station due to open in 2026; and Moneypoint’s coal and heavy fuel oil-powered operation is due to cease in 2024 to make way for a new renewable energy hub on the site.

Further changes will take place in sites such as Bord na Móna’s plant in Edenderry, where use of peat on a 118MW steam turbine will be phased out by 2024, a move which will see the turbine powered exclusively by biomass; and in Aghada, where a 90MW gas/distillate oil turbine is to be taken offline by the end of 2023.

NERI’s study shows that “the two power plants projected to cease operations completely… are both placed in the south-west of the island” and “within proximity to each other at the outer county borders of Clare and Kerry”. With Moneypoint and Tarbert, the plants in question deliver a “high volume of the electricity that is fed into the island-wide electricity grid”. It is then “reasonable to assume both plants are employing a significant proportion of workers” in the sector.

Changes in employment are likely to be “less disruptive” in Kilroot and Edenderry due to the plants continuing to generate electricity, the report states.

‘A troubling cocktail’

Such disruption and the possible job losses that it would cause “could present a troubling cocktail of factors impeding transition efforts” due to the fact that jobs in electricity generation are a “key source of well-paid employment at the bottom of the labour market” and those leaving the sector would “face worse prospects at similar job skill levels elsewhere in the economy” in both jurisdictions, the report states.

In both jurisdictions, “available data suggest that employment within the electricity sector is well paid in relation to the wider economy”, with weekly earnings in the relevant category found to be 35 per cent higher than the average weekly earnings in the Republic’s economy, and comparable data for Northern Ireland showing relevant wages to be between 9 and 11 per cent higher than the rest of the economy as a whole in both median and average terms.

The electricity sector also tends to show less of an earnings gap between top grade and other categories. In the Republic, while wages for managers, professionals, and associated professionals are typical 2.3 times the average of the wages of clerical, sales, and service employees, this figure falls to 1.7 in electricity; and in Northern Ireland, entry into the lowest quintile of workers in electricity required a weekly wage of less than £418.90, 46 per cent higher than the threshold for the economy as a whole, where the lowest quintile earns £286.20 or less per week.

Alongside its importance from a pay perspective, the sector is also vital to certain areas both north and south in terms of employment. Given that the sector comprises 0.5 per cent of aggregate employment across the Republic, NERI estimates a rate of 0.5 per cent employment in each council area, a rate that is significantly outstripped in areas such as Offaly (73.1 per cent), Kerry (21.5 per cent), and Clare (9.3 per cent). Fingal shows the highest level of overrepresentation in terms of total people employed, with 855 employed compared to an expectation of 770. A similar exercise carried out by NERI in Northern Ireland finds both Derry City and Strabane and Lisburn and Castlereagh to have significant overrepresentation in the sector, 50.1 per cent and 25 per cent respectively.

The importance of these well-paid and overrepresented jobs is brought into even sharper focus when contextualised within county/regional labour market indicators.

In Northern Ireland, while Lisburn and Castlereagh is the highest performing local authority area in terms of economic activity (78.4 per cent compared to an average of 73 per cent), Derry City and Strabane is the worst performing local authority area with a rate of 68 per cent.

In the Republic, the Dublin and Midlands region recorded labour force participation rates above the national average in the first quarter of 2023, but the west and southwest (where the soon-to-close Tarbert and Moneypoint plants are located) showed rates 1.1 per cent and 1.4 per cent below the 64.9 per cent national rate respectively.

When broken down into the county level, prominent counties within the electricity sector such as Offaly (2.2 per cent), Clare (1.8 per cent), and Kerry (3.1 per cent) register notable deficits against the national average.

Counties Offaly and Mayo, alongside Derry City and Strabane, are also noted within the reports as areas with fossil fuel generation that also record significant gross disposable household income figures below national averages; 14.6 per cent, 22.7 per cent, and 10.6 per cent respectively.

In Northern Ireland, poverty rates before and after the incorporation of housing costs average at 13 per cent and 18 per cent respectively; Lisburn and Castlereagh performs well in this area with averages of 11 per cent and 17 per cent, but Derry City and Strabane is again the worst performer in this area with rates of 20 per cent and 22 per cent.

In the Republic, the southern region underperforms against the national average in both the at-risk-of-poverty and enforced deprivation rates, while the eastern and midland region overperforms.

These stats, the report states, show “especially pronounced” risks for certain sites and their regions should job losses occur. Most notable among these sites are Moneypoint, Tarbert, and Coolkeeragh, which show risks across all factors measures, including broader labour market performance and poverty factors.

Other sites such as Contour Global, Edenderry, and Rhode show less risk, although NERI does warn in the case of the latter two that “this is likely an understatement of risk” given their location in Offaly, which is grouped together with Dublin in State statistics.

The statistics, the report says, “imply the sector presents a source of high-quality employment, particularly at the low end of the income scale” and that “transition plans must factor in these issues and respond accordingly”. Policymakers, NERI states, “should be attentive” to the challenges posed by their findings and “act to ensure that this transition is just”.