VAT and APD: No change

Potential cost to the exchequer, current tourism growth, EU law and the absence of a Northern Ireland Assembly are all contributing factors to the UK Government’s decision not to change the VAT rate on tourism related services or changing the current Air Passenger Duty regime.

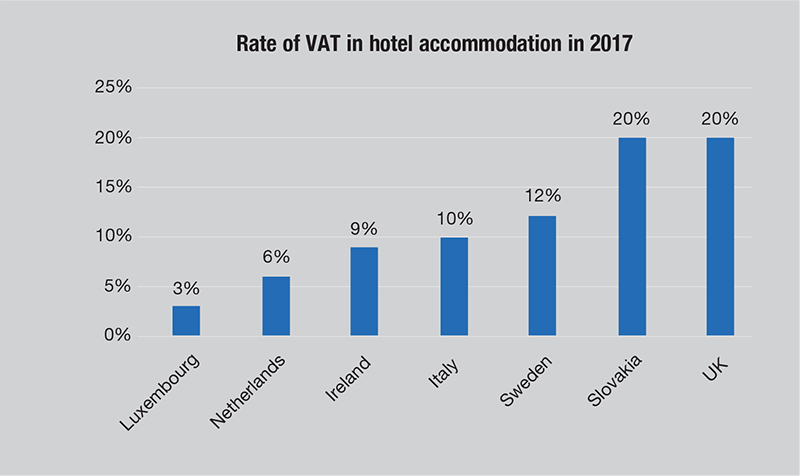

In 2017, a report commissioned by the Cut Tourism VAT campaign and carried out by Nevin Associates found that a cut of Northern Ireland’s VAT rate from 20 per cent to 5 per cent on hotels and visitor attractions could create over 2,000 new jobs in the region.

The report acknowledged that a cut in the rate would cost the Treasury over £4 million of income in the first year but argues that this initial cost would be superseded by a £32 million gain over five years and almost £110 million over 10 years.

The evidence from the report further fuelled long-standing calls for Northern Ireland to better compete with the Republic of Ireland, where VAT was reduced to 9 per cent in 2011 as a temporary stimulus for the sector at the height of the recession.

In January, Ireland increased the rate of VAT in the tourism and hospitality sectors to 13.5 per cent, still significantly lower than the rate in Northern Ireland.

On the back of concerns that Northern Ireland’s tourist industry has been particularly affected by Ireland’s low rate, the UK Government announced in the Autumn 2017 Budget that it would publish a call for evidence to “consider the impact of VAT and APD on tourism in Northern Ireland”. Published on 29 October as part of the 2018 Budget, the Government stated: “There will be no changes to the VAT or APD regimes in Northern Ireland at this time,” adding that it will continue to explore ways to support the industry.

A summary of the perceived benefits of VAT reduction includes:

- higher levels of employment generated, including increased wage levels and training;

- the increase of additional tax receipts as a result of additional employment and savings on social security payments;

- the increase of profits, corporation tax payments and shareholder dividends;

- improvement of industry and overall economic competitiveness; and

- increased spending in other sectors of the economy given tourism’s role as a multiplier.

The UK Government outlined its reasons for the decision not to initiate changes, including the challenges under a legal context. While Brexit may eventually change circumstances regarding the legal context for VAT, as it stands, current legislation (Principle VAT Directive) prevents the UK from offering different rates of VAT across the UK.

The UK does possess the ability to change the rate across all of its parts, as EU member states are permitted to maintain a reduced rate of VAT on tourism related services, including the likes of passenger transport, accommodation, attractions and food and beverage services. However, the Government believes that this would come at a “significant cost to the Exchequer”.

Even post-Brexit, it is unlikely that any Northern Ireland-specific action will be taken given that the Government is “committed to continuing the control of anti-competitive subsidies by creating a UK-wide subsidy control framework”. Such a move would involve a commitment to maintain a common rulebook with the EU on State aid, enforced by the Competition and Markets Authority.

The absence of an Executive in Northern Ireland also serves as a barrier. Tax devolution in Northern Ireland cannot take place until the restoration of Stormont as an Executive would have to take on responsibility of the devolved tax, meaning that any cost reduction in rate would result in a block grant adjustment.

VAT

Evidence in support of tax reform remains “inconclusive” according to the Government, which admitted that the majority of feedback to its call for evidence were in favour of creating unique circumstances for Northern Ireland.

As well as the legal context making it “impossible” for the Government to take exclusive VAT action for Northern Ireland, they argue that any potential benefits of such a move must be taken alongside other considerations.

The main consideration is that of the potential administrative burden brought about by the shift. Highlighting that the EU VAT law was intended to minimise these burdens, the Government states: “The complexity of VAT and the associated administrative burden will continue to be an important consideration, maintaining a VAT system that is as simple as possible for business and taxpayers.”

Another consideration is that of the UK’s current “high VAT registration threshold”, which omits a high percentage of businesses in the industry from VAT altogether and which contributes to “making the UK an attractive location for tourists and business”. The Government states that these other features of the tax system add further complexity to predicting the outcome of any tax reform.

It also takes a cautionary approach to predicted long-term Exchequer benefits such as job growth and increased consumer spending, stating: “Currently, there are near record high vacancies in the market and, in the current climate, it may not be the case that growth would be supported through labour market effects.”

The report highlights the importance of the £125 billion (2017–2018) revenue that VAT provides to the Government and how any loss in receipts resulting from a new relief would have to be balanced with increased borrowing, reduced public spending or increased taxation in other areas. It highlights that the majority of evidence points to a short to medium term fall in VAT receipts.

Ireland’s tourism performance following the reduction of its VAT rate is often used as a comparative example of how such a move can boost the economic return. However, the Government argues that such analysis lacks context. It highlights that the 2011 introduction coincided with high unemployment and scope for growth, believing that growth in Ireland has reflected global economic recovery. “The evidence around the scale of impact of price reductions remains inconclusive,” the report states.

On VAT, the report concludes: “While there may be scope to make changes in the future, this is a complex area affecting important sources of revenue for the Exchequer which requires further exploration.”

APD

In terms of aviation, Northern Ireland’s unique position, in sharing a land border with the EU, has recognisable ramifications for competition in the market. Again, the UK highlights an inability to vary rates for different regions within EU law on State aid and adds that further tax devolution is not possible without an Executive in place.

“Abolishing APD across the whole of the UK is possible in the current legal framework, however the tax raises approximately £3.5 billion per year for the Exchequer. Abolishing or cutting APD at a UK level would have to be balanced by increased borrowing, reduced public spending or increased taxation elsewhere,” the report explains.

The report states that it is “not clear” that changes to APD would be the most cost-efficient and effective way for the Government to support the tourism industry. The Government has set out to establish a technical working group to consider the practical and legal challenges to changing short-haul APD in Northern Ireland, but concluded: “Due to the current legal constraints, the government will not be taking forward any changes to the APD regime in Northern Ireland at this time.”